Understanding Presumptive Taxation: Do You Need ITR 3 or ITR 4?

Understanding Presumptive Taxation: Do You Need ITR 3 or ITR 4?

Managing taxes in India can often feel like solving a complex puzzle, especially when it comes to picking the right tax form. At GST Wale, we interact with hundreds of small business owners and professionals every year who get stuck at the final step of the process. Whether you are a freelancer, a consultant, or a business owner, knowing the difference between your options is key to compliance. If you are struggling with your annual compliance, our professional ITR Filing service is here to ensure you stay error-free. One of the most common dilemmas we encounter is deciding whether you should file itr 3 or if you can opt for the simpler route provided by ITR 4.

The Presumptive Taxation Scheme: A Quick Overview

Before we dive into the specific forms, let’s talk about the "shortcut" many small businesses love. The Presumptive Taxation Scheme under Sections 44AD, 44ADA, and 44AE is designed to reduce the compliance burden. Instead of maintaining exhaustive books of accounts and getting them audited, you pay tax on a "presumed" percentage of your income.

If you opt for this scheme, you are generally required to use ITR 4. However, the catch is that this scheme isn’t for everyone. If your business nature, turnover, or specific financial events fall outside these boundaries, you must pivot to filing itr 3.

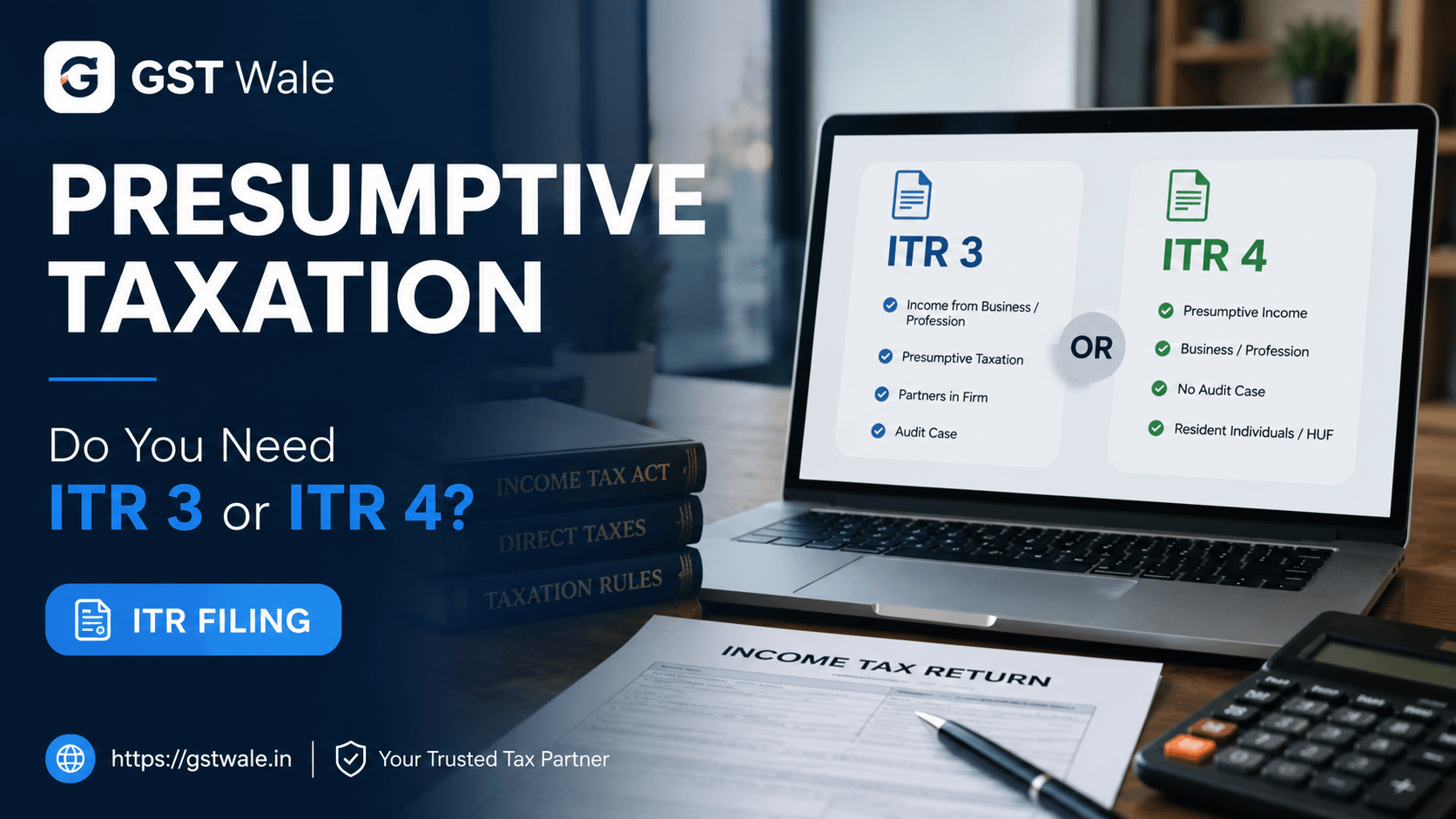

Decoding ITR 4 vs. ITR 3: Which One Is For You?

Choosing the right income tax return form is not just about convenience; it is about accuracy. Using the wrong form can trigger a notice from the Income Tax Department.

When to File ITR 4 (Sugam)

ITR 4 is the go-to for small taxpayers who have opted for the presumptive taxation scheme. You are generally eligible for this if:

You are an individual, HUF, or a firm (other than an LLP).

Your total income includes business income calculated under sections 44AD or 44AE, or professional income under section 44ADA.

Your total income does not exceed ₹50 lakhs.

When Must You File ITR 3?

If you don’t fit the criteria above, itr 3 becomes your mandatory choice. Think of it as the "all-inclusive" form for business owners and professionals. You must use itr 3 if:

You have income from a business or profession and you are NOT opting for the presumptive taxation scheme.

You are a partner in a firm.

You have income from speculative business or house property.

You have capital gains or income from "other sources" like lottery or horse racing.

Your annual turnover exceeds the limits specified for presumptive schemes.

Essentially, if your financial life involves complex entries, multiple sources of income, or if you simply prefer to report your actual profits after deducting expenses, itr 3 is the form designed for your needs.

Why Some Businesses Move Away from Presumptive Taxation

At GST Wale, we often advise clients that while presumptive taxation (ITR 4) is easy, it isn't always the most tax-efficient route. Here is why you might decide to file itr 3 instead:

High Expenses: If your actual profit margin is significantly lower than the "presumed" percentage (e.g., 6% or 8% under section 44AD), you are paying tax on money you didn't actually earn. By filing itr 3, you can claim your actual business expenses and reduce your tax liability.

Maintaining Records: If you are planning to take a large business loan, banks prefer to see properly maintained books of accounts. Filing under itr 3 allows you to show your transparent financial health.

Nature of Business: Certain businesses are legally excluded from presumptive schemes. If you fall into those categories, itr 3 is your only legal option.

Common Mistakes to Avoid During IT Filing

When you file it returns online, the smallest error can lead to a delay in processing your refund. From our experience, here are the most frequent slips:

Mismatch in TDS: Ensure that the TDS reflected in your Form 26AS matches the income you are declaring in your itr form.

Ignoring Income Sources: People often forget to report savings bank interest or small dividend income, thinking it's insignificant. Report everything.

Choosing the Wrong Form: Selecting ITR 4 when you have capital gains from the stock market is a classic mistake. If you have any capital gains, you must graduate to itr 3.

Frequently Asked Questions (FAQs)

1. Can I switch from ITR 4 to ITR 3?

Yes, you can choose to move away from the presumptive scheme and file itr 3 if you believe your actual profits are lower or if your business structure has changed.

2. Is audit mandatory if I file itr 3?

Not always. An audit is only mandatory under Section 44AB if your turnover exceeds specific thresholds (usually ₹1 crore for businesses, extendable to ₹10 crores under certain conditions) or if you report a profit lower than the presumptive rate.

3. Does filing itr 3 increase my chances of scrutiny?

Not necessarily. As long as your disclosures are accurate and match your Form 26AS and AIS (Annual Information Statement), you have nothing to fear.

4. Can I file incometax return online by myself?

You can certainly try, but tax laws in India change rapidly. For those with complex business income, consulting a professional ensures you don't miss out on eligible deductions.

Expert Guidance from GST Wale

Taxation is not just about filing; it is about planning. Whether you need to file itr 3 or want to verify your eligibility for the presumptive scheme, the team at GST Wale is here to simplify the complexities for you. We provide end-to-end support for all your tax compliance needs, ensuring that you remain tax-efficient while staying 100% compliant with the Income Tax Act.