How to Claim Maximum Deductions Under Section 80C in ITR 2.0

How to Claim Maximum Deductions Under Section 80C in ITR 2.0

Every year, as the tax season approaches, taxpayers start looking for ways to reduce their taxable income legally. Navigating the complex landscape of tax laws can feel overwhelming, but with the right guidance, it becomes manageable. At GST Wale, we believe that informed planning is the key to financial freedom, which is why we offer comprehensive ITR Filing services to ensure you remain compliant while optimizing your tax liability. When you are preparing to submit your itr 2.0, understanding the nuances of Section 80C is the first step toward significant savings.

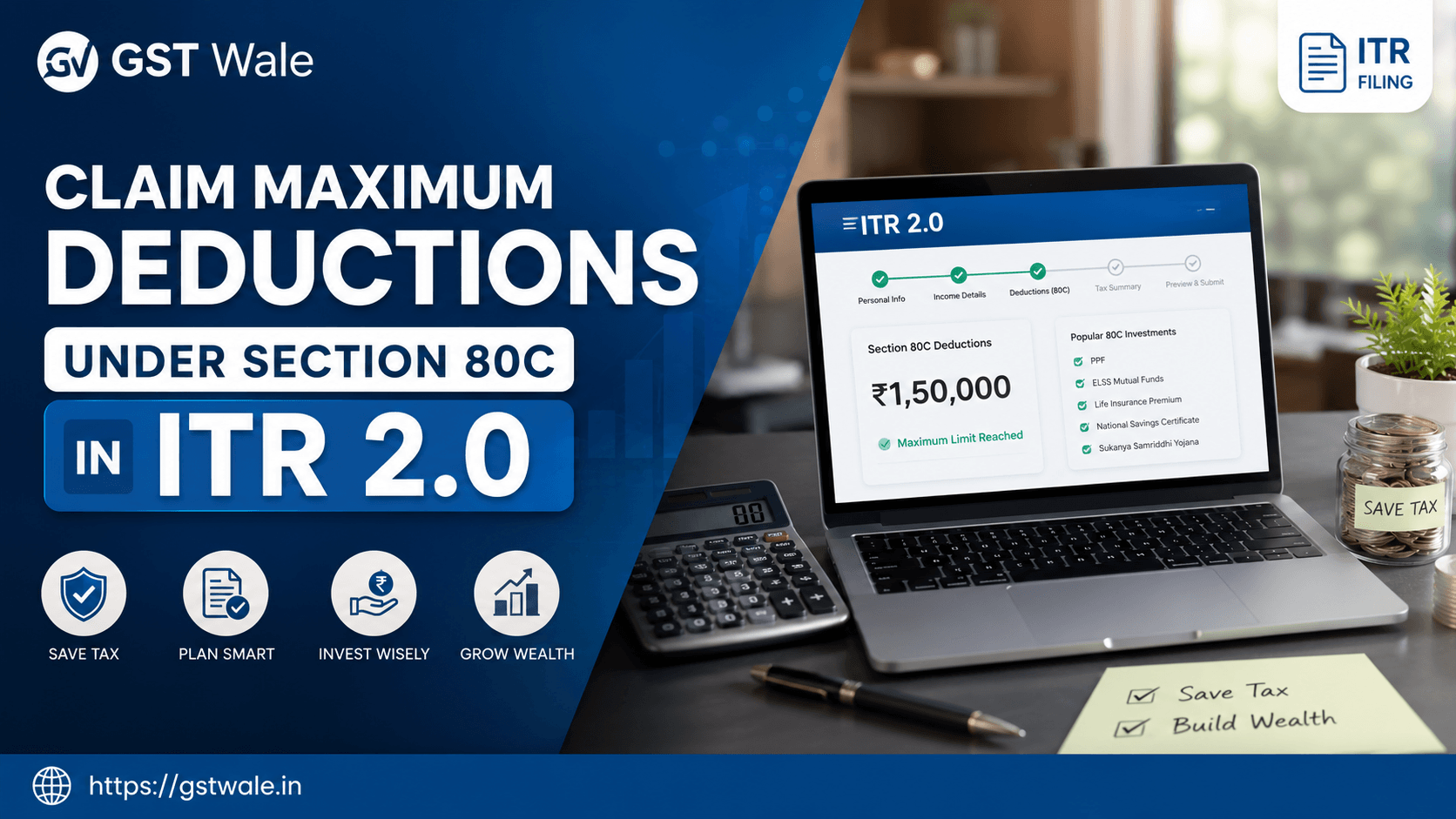

Section 80C of the Income Tax Act is undoubtedly the most popular tax-saving provision in India. It allows individuals and HUFs to reduce their taxable income by up to ₹1.5 lakh in a financial year. While many taxpayers are aware of the limit, they often miss out on the best combinations of investments. As you prepare your itr 2.0, let’s break down how you can maximize these deductions strategically.

Understanding the Power of Section 80C Deductions

Section 80C is not just a tax-saving tool; it is a discipline for wealth creation. When you claim these deductions in your itr 2.0, you are essentially paying yourself first while lowering your tax outgo. The limit of ₹1.5 lakh is a combined limit, meaning it encompasses several different investment avenues.

To claim these benefits, you must ensure your investments are made within the relevant financial year. Whether you choose itr 2 or other forms based on your income sources, the documentation remains crucial.

Top Investment Avenues to Maximize Section 80C

To get the most out of your itr 2.0 filing, you need to mix and match your investments. Here are the most effective instruments:

Public Provident Fund (PPF): A long-term favorite. It offers tax-free interest and is backed by the government, making it one of the safest bets.

Equity Linked Savings Scheme (ELSS): These are tax-saving mutual funds with the shortest lock-in period of just three years. They have the potential to deliver better inflation-adjusted returns compared to traditional debt instruments.

National Savings Certificate (NSC): A fixed-income scheme with a five-year lock-in. It is ideal for those who prefer guaranteed returns.

Life Insurance Premiums: Premiums paid for yourself, your spouse, or your children are eligible for deduction.

Children’s Tuition Fees: You can claim deductions for the tuition fees paid to any university, college, or school in India for up to two children.

Principal Repayment of Home Loan: If you have an active home loan, the principal portion of your EMI payments qualifies under Section 80C.

Practical Tips for Your ITR 2.0 Submission

When you sit down to file your itr 2.0, precision is key. Many taxpayers lose out on potential savings due to simple clerical errors.

1. Maintain Meticulous Records

Before you start your itr form completion, gather all your investment proofs. Keep your LIC receipts, bank statements, and tuition fee certificates handy. When you file income tax return online, having these documents digitally prepared speeds up the process significantly.

2. Don’t Ignore Other Sections

While Section 80C is great, don't forget that it filing involves other sections too. For instance, premiums paid for health insurance can be claimed under Section 80D, which is over and above the 80C limit. Smart tax planning looks at the entire income tax return form holistically.

3. Timing Matters

Often, people rush their investments in March, the last month of the financial year. This "last-minute panic" often leads to poor investment choices. Try to plan your investments systematically throughout the year so that your itr 2.0 reflects a well-thought-out financial strategy.

Common FAQs About 80C and ITR Filing

Can I claim 80C deductions if I opt for the New Tax Regime?

No, the New Tax Regime does not allow most deductions, including Section 80C. You can only claim these benefits under the Old Tax Regime.

Is the ₹1.5 lakh limit per head or per family?

The limit applies to each individual taxpayer. In a family, if both husband and wife are earning, both can individually claim the ₹1.5 lakh deduction in their respective itr 2.0 filings.

What happens if I forget to declare 80C investments while filing?

If you miss declaring them in your original return, you may need to file a revised return to claim the deduction, provided the timeline for filing a revised return hasn't expired.

Does EPF contribution count towards 80C?

Yes, the mandatory employee contribution to the Employees' Provident Fund (EPF) is eligible for deduction under Section 80C.

Tax planning is an ongoing process, not a one-time activity. While Section 80C is a fantastic way to lower your tax liability in your itr 2.0, ensure that your investments also align with your long-term financial goals—like buying a house, funding your child’s education, or building a retirement corpus.

At GST Wale, we understand that navigating the nuances of the itr form can be stressful. We are here to handle the complexities for you. Whether you are confused about which itr 2 provisions apply to you or you need expert assistance to file income tax return online without errors, our team of experienced CAs is just a call away.