A Jeweller’s Manual: How to Issue a Compliant Tax Invoice for GST for Gold Purchases

A Jeweller’s Manual: How to Issue a Compliant Tax Invoice for GST for Gold Purchases

Running a jewelry business in India is as much about trust as it is about craftsmanship. When a customer walks into your showroom, they aren’t just buying an asset; they are investing their hard-earned money into something precious. However, as a jeweler, your responsibility doesn't end when the ornament is weighed and packaged. The real challenge begins at the billing counter. Navigating the rules of gst for gold can feel overwhelming, especially with complex calculations involving making charges, stone values, and old gold exchanges.

At GST Wale, we interact with hundreds of jewelers who often struggle with compliance. Missing a minor detail on a tax invoice can lead to heavy penalties during a departmental audit. If you are a new jeweler setting up your showroom or an established businessman looking to streamline your compliance, getting your legal basics right is crucial. The very first step to operating legally is securing a valid GST Registration, which acts as the foundation of your tax compliance journey. Once registered, your primary daily task is ensuring that every single transaction is recorded flawlessly.

In this comprehensive manual, we will break down exactly how to issue a compliant tax invoice for gold purchases, ensuring your business stays 100% compliant.

Understanding the GST Rates Structure for Jewelry

Before we jump into the gold invoice format, let’s clarify the current tax rates applicable to the jewelry industry. Jewelry billing isn't a single-line calculation; it involves different components taxed under specific guidelines.

Here is a quick snapshot of the gst rates applicable today:

Gold Bullion and Jewelry: A flat 3% GST is levied on the value of gold.

Making Charges: Making charges represent job work. If a jeweler manufactures jewelry in-house or outsources it, the making charges attract a 5% GST if billed separately, but when sold as an item of jewelry, the entire composite supply is taxed at 3%.

Precious Stones: Diamonds, rubies, and emeralds embedded in the jewelry attract the same 3% GST when sold as a part of the jewelry piece.

Expert Note from GST Wale: In the jewelry business, selling an ornament is considered a Composite Supply. This means the gold, the making charges, and the stones cannot be naturally separated in the final product. Therefore, the principal supply is gold, and the entire invoice value (including making charges) is taxed at the primary rate of 3%.

Step-by-Step Breakdown of a Compliant Gold Invoice

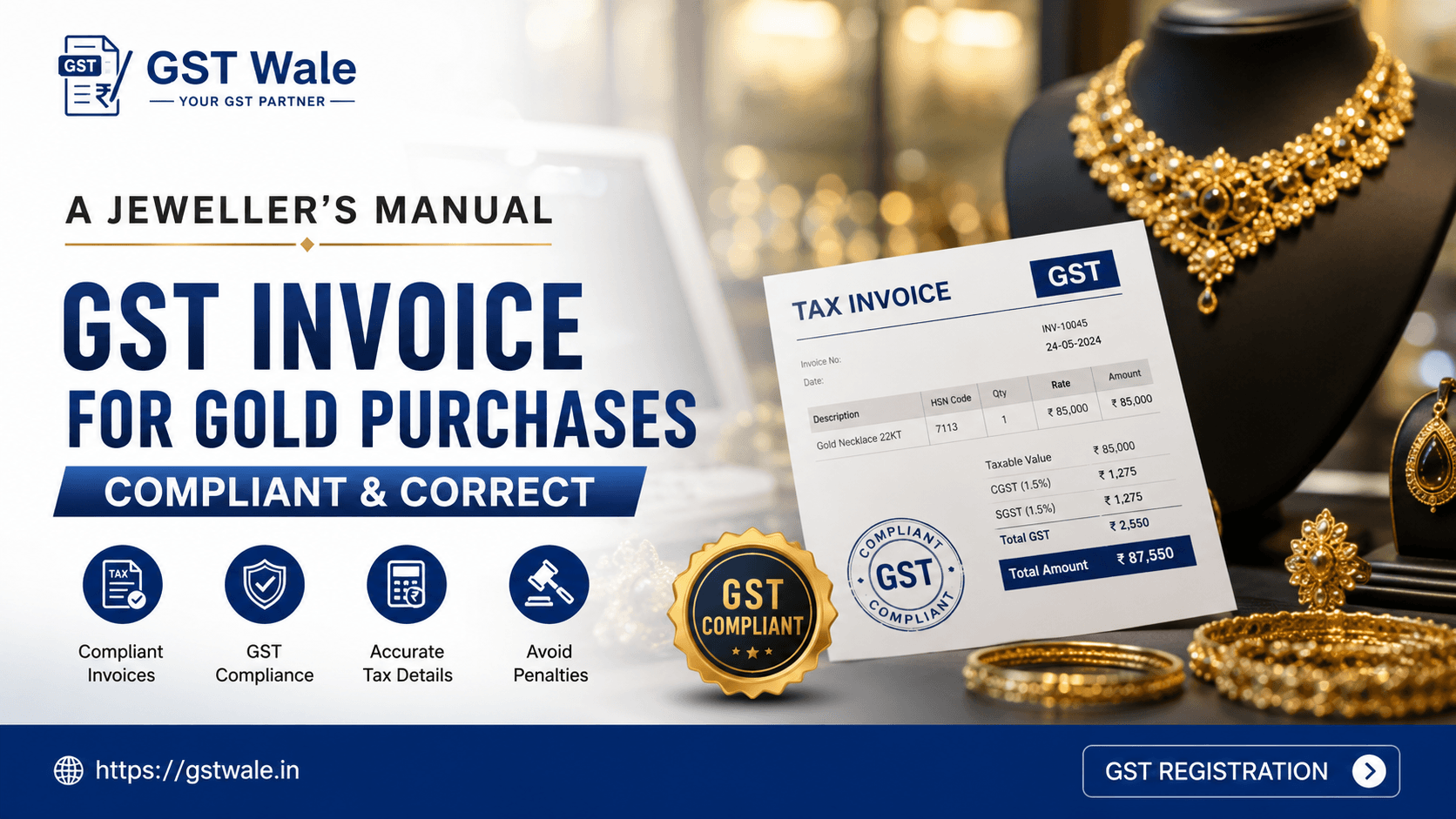

To ensure your billing software or physical bill book complies with the law, every tax invoice must contain specific mandatory fields. Let’s look at how you should structure your invoice.

1. Header and Basic Details

Every invoice must clearly display your business credentials. This includes your brand name, legal business name, address, and your 15-digit GSTIN. The document must explicitly state "Tax Invoice" at the top. You must also maintain a consecutive, unique serial number for every financial year.

2. Customer Details (B2B vs. B2C)

Gold B2C Billing: For regular retail customers, you need their name and address. If the invoice value exceeds ₹50,000, collecting their PAN card details is highly recommended to comply with anti-money laundering guidelines.

B2B Billing: If you are selling to another registered trader or jeweler, you must mandate their GSTIN and correct state code to pass on the Input Tax Credit (ITC).

3. HSN Codes and Item Description

You cannot simply write "Gold Ring" and put a price tag. The government requires specific Harmonized System of Nomenclature (HSN) codes:

7108: For Gold (including gold plated with platinum), unwrought or in semi-manufactured forms.

7113: For Articles of jewelry and parts thereof, of precious metal.

The Math Behind the Invoice: Breaking Down Pure Gold Value

Let's look at a practical example. Suppose a customer buys a gold chain weighing 10 grams. The market rate of 24k gold is ₹7,000 per gram, but the chain is made of 22k gold.

When preparing the invoice, you must show transparency by breaking down pure gold value. The invoice should clearly state:

Gross Weight of the article.

Net Weight of the gold (excluding stones or lac).

Purity of the gold (e.g., 22 Carat / 916 Hallmarked).

The Making Charges Split

Many jewelers ask us whether they should show the making charges separately. The answer is yes. Displaying a clear making charges split creates transparency for the customer and protects you during tax assessments.

Here is how the calculation works under the composite supply rule:

| Component | Value Calculation | GST Rate | GST Amount |

|---|---|---|---|

| Gold Value (22k) | 10 grams x ₹6,500 = ₹65,000 | 3% | ₹1,950 |

| Making Charges | ₹500 per gram = ₹5,000 | 3% (Composite) | ₹150 |

| Total Value | ₹70,000 | 3% | ₹2,100 |

The total tax on gold items in this scenario equals ₹2,100 (split equally into 1.5% CGST and 1.5% SGST for intrastate sales). The final amount payable by the customer will be ₹72,100.

Handling Old Gold Exchanges: The Tax Implication

One of the most common practices in Indian jewelry stores is customers exchanging old gold ornaments for new ones. How do you reflect this on your invoice?

Treat it as a Separate Transaction: The purchase of old gold from an unregistered consumer is technically an inward supply.

No RCM on Public Purchases: According to clarification issued by the CBIC, buying old gold from an individual consumer does not attract Reverse Charge Mechanism (RCM) because the individual is not selling it in the course of business.

Invoice Adjustment: In your final invoice, calculate the full value of the new jewelry, apply the 3% gst for gold, and then deduct the valuation of the old gold as an advance payment or trade-in discount code.

Checklist for a Perfect Gold Invoice Format

To avoid mistakes, double-check that your invoicing system includes these fields:

[ ] HSN Code (7113 for jewelry) clearly mentioned.

[ ] Separate columns for Gross Weight, Waste, Net Weight, and Purity.

[ ] Clear bifurcation of CGST (1.5%) and SGST (1.5%) or IGST (3%).

[ ] Hallmark charges (if applicable) mentioned as a separate line item.

[ ] Digital signature or physical signature of the authorized signatory.

Frequently Asked Questions (FAQs)

Q1. Is GST applicable on making charges of gold jewelry?

Yes, gst in gold billing applies to making charges. When you buy ready-made jewelry, the making charges are part of a composite supply and are taxed at 3%. However, if you hand over your own gold to a goldsmith for job work, the goldsmith will charge 5% GST on their labor invoice.

Q2. What happens if I fail to mention the HSN code on the invoice?

Failing to mention the correct HSN code or using incorrect gst rates can attract a penalty under Section 125 of the CGST Act, which can go up to ₹25,000 per error, alongside potential charges for misdeclaration during audits.

Q3. Can a B2C customer claim Input Tax Credit on gold purchases?

No. Retail consumers purchasing gold for personal use cannot claim Input Tax Credit. ITC can only be claimed by registered businesses purchasing gold for furtherance of business (like a retailer buying from a wholesaler).

Q4. Are hallmark charges subject to GST?

Yes, hallmarking is a service provided to certify purity. It attracts standard service tax rates, but when passed on to the final customer as part of the jewelry sales invoice, it is taxed at the primary rate of 3%.

How GST Wale Can Protect Your Jewelry Business

Compliant billing is the shield that protects your business from sudden tax notices. As the government tightens its grip on the gold sector with e-invoicing mandates and stricter matching rules, manual errors are no longer an option.

At GST Wale, we specialize in helping jewelers set up flawless accounting systems, file error-free returns, and navigate complex departmental audits. Let us handle the tax complexities while you focus on designing stunning masterpieces for your clients. Reach out to our team at GST Wale today for expert accounting and compliance support!